Income splitting in Canada is a tax planning strategy that involves transferring income to family members in lower tax brackets to reduce overall tax liability and maximize savings.

But income splitting is more than just a tax strategy. For Canadian business owners, it can also be a way to support family members financially while optimizing taxes.

By sharing income with family members in lower tax brackets, you can take advantage of Canada’s progressive tax system, which taxes higher income at higher rates. Proper income splitting can reduce your total family tax burden and help your loved ones achieve their financial goals.

In this guide, we explore eight practical income splitting strategies every Canadian business owner should understand.

Who Is Eligible for Income Splitting in Canada?

Income splitting typically benefits business owners who earn significantly more than their family members.

Eligible recipients of split income may include:

- Your spouse

- Adult children

- In some cases, minor children

However, income splitting must comply with the Tax on Split Income (TOSI) rules.

Understanding the TOSI Rules

The Tax on Split Income (TOSI) rules were introduced to prevent unfair tax advantages through income splitting.

Under TOSI, certain types of income are taxed at the highest marginal tax rate (about 53.5%).

TOSI can apply to:

- Taxable dividends

- Capital gains

- Income from partnerships or trusts

Fortunately, there are several legitimate strategies where TOSI does not apply or can be minimized.

1. Pay Dividends to Family Members Who Work in the Business

One effective strategy is paying dividends to family members who actively work in the business.

To qualify:

- The individual must be 18 years or older

- They must work at least 20 hours per week on average

- You must maintain timesheets and records

- Payments must be reasonable based on the job performed

If these conditions are met, the dividends are generally not subject to TOSI.

2. Pay Dividends Through an Excluded Business

Another strategy is paying dividends to family members who own shares in an excluded business.

To qualify as an excluded business:

- Less than 90% of revenue comes from services

- The family member owns at least 10% of the company’s shares (votes and value)

- The individual is 25 years or older

- The business is not a professional corporation (e.g., doctor, lawyer, accountant)

This strategy works well for businesses such as:

- Retail stores

- Manufacturing companies

- Restaurants

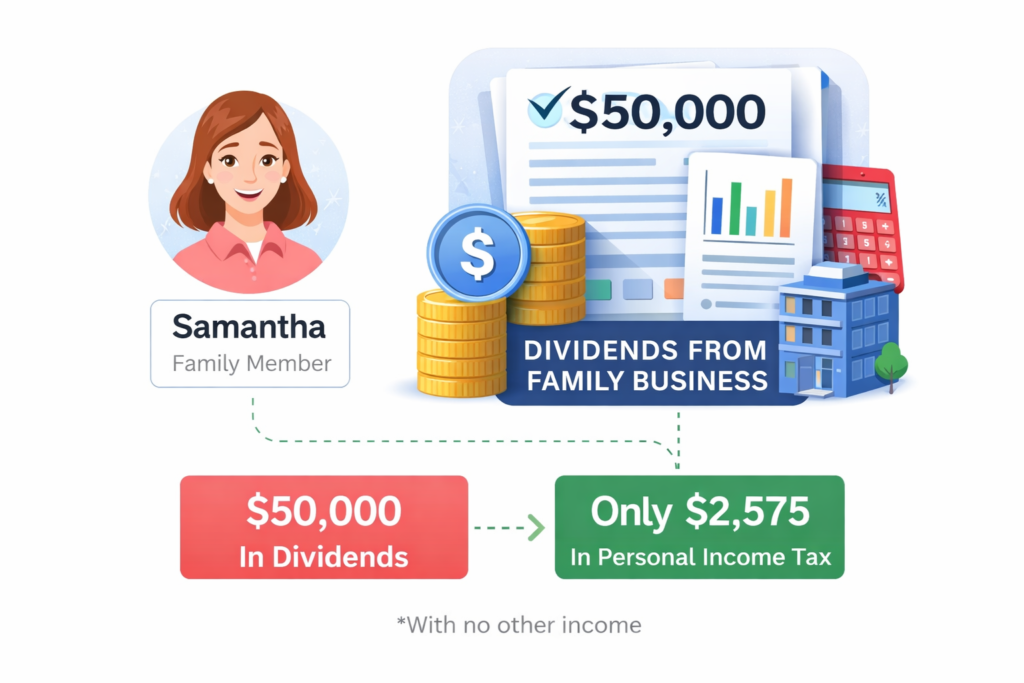

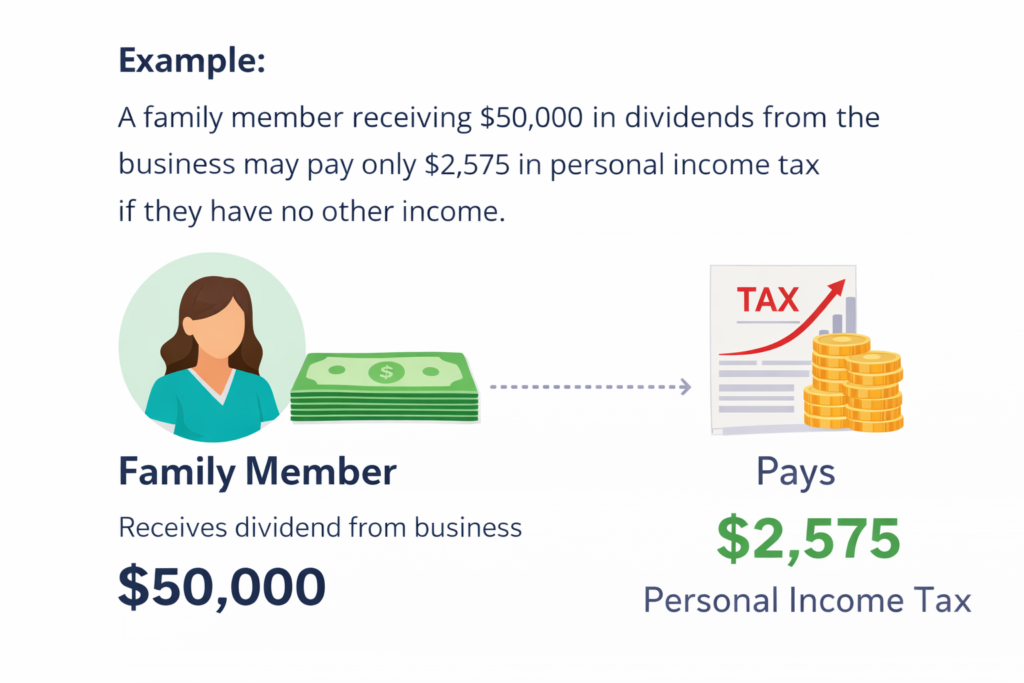

Example:

A family member receiving $50,000 in dividends from the business may pay only $2,575 in personal income tax if they have no other income.

3. Pay Salary to Family Members Working in the Business

You can also pay a salary to family members who work in the business.

The salary must be reasonable based on the role and hours worked to be considered a deductible expense.

It’s recommended to have:

- A formal employment agreement

- Clear job responsibilities

- Accurate timesheets

Example:

If a business owner pays their daughter $40/hour for administrative work where the market rate is $18/hour, the company may lose a small deduction. However, the overall family tax savings could still be significant.

4. Spousal RRSP Contributions

Spousal RRSP contributions allow high-income earners to contribute to their spouse’s retirement account.

Benefits include:

- Lower overall family taxes in retirement\

- Balanced retirement income between spouses

- Reduced tax burden for high earners

5. Use a Registered Education Savings Plan (RESP)

RESP contributions can also help with income splitting.

Benefits include:

- Saving for your child’s education

- Government matching through the Canada Education Savings Grant (CESG)

- Withdrawals are taxed in the student’s name, typically at a lower tax rate

The government matches 20% of contributions, making it a powerful tax and savings tool.

6. Multiply the Lifetime Capital Gains Exemption

When selling a business, income splitting can multiply the Lifetime Capital Gains Exemption (LCGE).

Currently, individuals can claim up to $1.25 million in tax-free capital gains.

Using a family trust, multiple family members may claim the exemption.

Example:

A family of four selling a $5 million business could potentially avoid taxes on the entire gain.

7. Share Ownership of Investment Corporations

If you hold investments or real estate in a corporation, family members can own shares.

Dividends are then distributed according to each shareholder’s personal tax bracket.

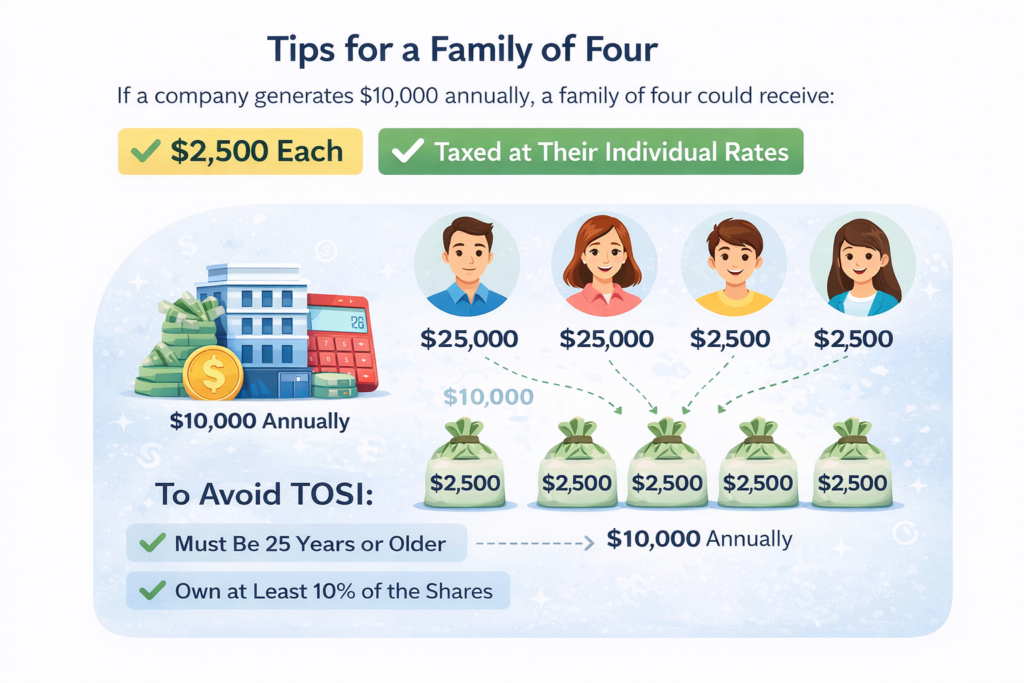

Example:

If a company generates $10,000 annually, a family of four could receive:

- $2,500 each

- Taxed at their individual rates

To avoid TOSI:

- The individual must be 25 years or older

- They must own at least 10% of the shares

8. Gift Personal Assets to Your Children

Gifting personal assets such as land, gold, or other investments can also shift future capital gains to your children.

Since your children may be in lower tax brackets, the capital gains tax could be significantly reduced.

Final Thoughts

Income splitting in Canada is a powerful strategy for Canadian business owners looking to reduce taxes and support their families financially.

From paying salaries to leveraging the lifetime capital gains exemption, the right strategy depends on your business structure and financial goals.

Before implementing any income splitting plan, it’s best to consult a tax professional to ensure compliance with CRA rules and TOSI regulations.

Learn More: 2025 Canadian Tax Season: Key Deductions and Credits You Shouldn’t Miss

Frequently Asked Questions

What is income splitting in Canada?

Income splitting is a tax strategy where income is distributed among family members in lower tax brackets to reduce the overall tax burden.

What is the TOSI rule?

TOSI (Tax on Split Income) prevents unfair tax advantages by taxing certain split income at the highest marginal tax rate.

Can I pay my children from my business?

Yes, if they genuinely work in the business and receive a reasonable salary based on their duties.

How can a family trust help with income splitting?

A family trust can distribute capital gains among beneficiaries, allowing multiple family members to use the lifetime capital gains exemption.